Financial Independence ratio: the measurement for quitting your day job

The general definition of financial independence (FI) is when you have enough passive income to cover your living costs. Needless to say, living costs are subjective; so for the purposes of clarity, I believe the definition of living costs in relation to FI should be essential costs only.

This should be the minimum you need to survive on; Netflix, alcohol, eating-out won't cut it! With an objective denominator, it's possible to calculate a simple FI ratio. An FI ratio is a lot more telling than "fat" or "lean fire". Moreover, knowing your absolute minimum living cost denominator is a useful metric to have.

My Financial Independence denominator

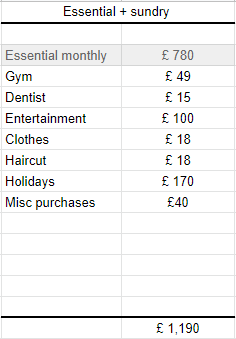

Listed below are my absolute essential running costs that make up my FI denominator. Although not part of my current plan; I estimate my essential living costs could be optimised by a further £100 if I moved home as this could lower council tax, service charge, ground rent and buildings insurance. It's also worth noting that this really is barebones as doesn't account for clothes or the dentist.

Regardless of how much I dislike my current job, if I give up work when I have enough passive income to cover living costs only then it's fair to say my life would become worse. I like to buy books, have a drink, go on holiday - who doesn't? So how much is enough?

Financial Independence happiness ratio

With essential costs calculated it's now a simple case of adding in non-essential costs that make early retirement enjoyable. Here are mine:

With the addition of £410 and using my FI number of £780, this makes my FI target ratio: 3:2 or 150%. This feels like a sensible target to aim for where I can still do the things I currently enjoy without feeling like I'm living on the breadline.

Working ad hoc

I plan to work sporadically or part-time but undecided on what yet, obviously this influences when you quit your day job and changes your FI ratio. So with all I've said, quitting with FI money only is doable if the plan is to earn supplementary income.

Based on the numbers above, I'd need ~£400 per month to turn a basic existence (100% FI) into an enjoyable one (150%). Using an hourly rate of £10 for an average part-time job in London, this would mean working 10 hours per week. Anyway, these are all options to consider. I'm sure like most people though, I feel more secure with some buffer and feel that sits somewhere between 20-40% above FI.